DISCLOSURE: THIS POST MAY CONTAIN AFFILIATE LINKS,MEANING That I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS, AT NO COST TO YOU. PLEASE READ FULL DISCLOSURE HERE

So, is art investing with Masterworks a good investment?

Can you really get better returns than stocks or bonds?

Can art investments truly diversify your portfolio and lower your risks?

How Masterworks Works

Masterworks is the first platform that allows investors to buy and sell shares representing an investment in artworks.

Here’s how it works.

Masterworks’ research teams select artists whose art has the most potential to appreciate over time, then buy art from them.

After that, they file an offering circular with the Securities and Exchange Commission, so anyone can invest in the artwork by buying shares.

It works kind of like an IPO where you buy shares in the underlying business.

Instead of buying shares in a business, you are buying shares in an artwork.

On its website, it says that they typically wait for 3 to 10 years until they sell the painting. Then you can receive your pro rata proceeds, after their fees.

If you want to get out, you can also sell your shares on their secondary market.

However, they cannot guarantee that there is enough liquidity or effective valuation of your shares.

So, is it really worth investing in art?

Let’s go through the Pros and Cons of art investing through Masterworks as well as ALL THE RISKS in investing in art.

Masterworks Art Investing Pros & Cons

Let’s first look at all the downsides of Masterworks art investing because it’s always wise to consider all the risks before investing your hard-earned money in something.

First of all, art is illiquid.

It’s much more illiquid than real estate.

That means if you want to sell your art pieces, it might take a very long time because there aren’t a lot of ready buyers.

There is also the possibility of never being able to find a buyer at a reasonable price.

Illiquidity risk leads to another risk which is pricing.

As the art market is not transparent, large, and liquid like the stock market, you will find it very difficult to value your art pieces.

In the stock market, the stock price is updated in real-time, and you can easily know how much your stock is valued.

With art, you don’t have that.

On top of that, there is no clear (and standard) way of valuing an art piece.

So, it really comes down to how much the buyer thinks the art piece is worth to him.

Personally, I feel uncomfortable about this.

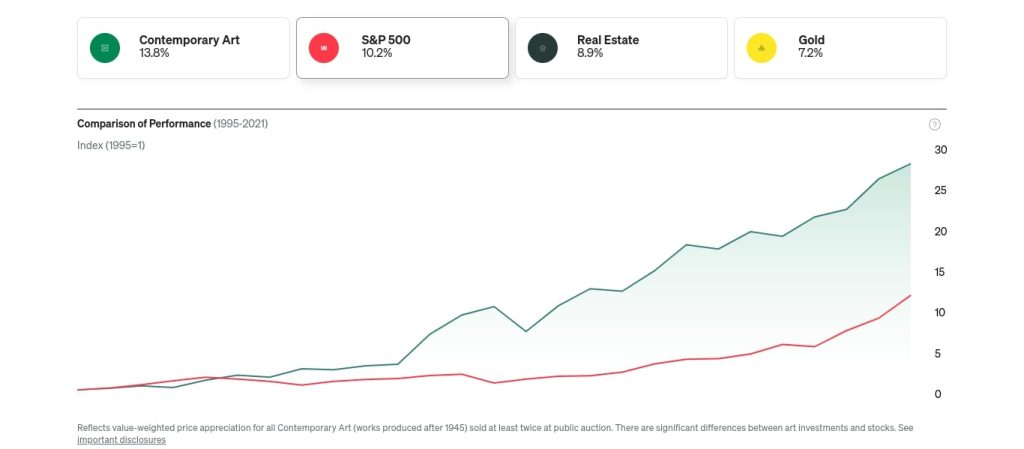

If you do an online search about art investing, you will see some articles that talk about how art outperforms the stock market as an asset class.

By the way, the data they cited in the article comes from Masterworks.

In fact, if you go to Masterworks’ website, you can see the performance comparison chart as shown below.

Based on Masterworks’ data, art clearly is better than stocks, real estate, and gold as an asset class.

But, can this data be trusted and relied on to make decisions?

Below is the important disclosure made by Masterworks regarding the data.

“Compiling meaningful price appreciation data for artwork is inherently difficult and prone to a number of significant limitations and subjectivity that significantly limit the utility of such data in evaluating future appreciation rates. Difficulties arise due to the unique nature of each painting, coupled with the fact that paintings tend to sit in collections for many years, if not several decades, which most often makes it impossible to find sufficient recent actual sales data to establish an appreciation trend line. To try to estimate how much a specific painting has appreciated over time often requires extrapolation to sales data from a set of similar works by the same artist. The selection criteria for what constitutes a “similar” work are highly subjective and even experts would likely disagree on exactly which particular works or characteristics, such as size, colors, subject matter, condition, etc. should be included or excluded in any given comparative data set. The level of subjectivity involved differs depending on the uniqueness of the underlying artwork. Furthermore, private sales data, which includes a majority of sales, is often unavailable or inaccurate, so the data set is typically comprised of only public auction sales data. The availability of public auction data varies by artist. As a general matter, a larger data set is more useful than a smaller data set. There can be no assurance that an investment mix or any actual price performance shown on the Site will lead to the expected results shown or perform in any predictable manner. It should not be assumed that investors will experience returns in the future, if any, comparable to those shown or that any or all investors on the Site experienced such returns.”

To summarize, it basically says that it’s extremely difficult to collect and compile art price data.

First of all, data is very limited.

Also, all the data is prone to subjectivity when it comes to selection criteria.

On top of that, transactions for the same artwork are few over a long period of time, so there is not enough actual sales data to establish the price appreciation trend line.

Masterworks even acknowledges that the utility of such data is significantly limited due to the above reasons.

Furthermore, it says that ” such historical data for a selected group of artwork should not be relied upon as an accurate comparison.” because each artwork is unique and has its own unique volatility and results.

So, at the end of the day, it comes down to whether or not the Masterworks team is good at finding art pieces that can appreciate over time.

However, when it comes to investing, there are always risks.

The value of the painting can go down.

So, investors should be prepared to lose all or a significant amount of their investments.

Even if the value of the artwork appreciates, it might not be enough to cover costs and expenses.

This is because there are a lot of fixed costs and fees involved such as financing fees and administrative service fees payable to Masterworks, and variable costs such as Masterworks profit sharing and third-party costs to sell the painting.

So, while your painting sits there, you are already bleeding money every day.

When you add up all these fees and costs over time, it could significantly reduce your total returns (if there is any positive return at all).

You must be aware that Masterworks has Potential Conflicts of Interest.

Masterworks charges a 1.5% annual management fee.

So, it could be incentivized to get as many investors as possible and launch as many offerings as possible.

Regardless of whether the painting appreciates or not, Masterworks still makes money from its management fees.

This fee is deducted from the investors’ equity.

In other words, the number of shares that you own decreases every year.

Lastly, Masterworks performs internal valuations of artwork held by Masterworks issuers as opposed to obtaining valuations from independent third parties.

So, the valuation of your art investment is not independently verified.

Essentially, you buy some artwork from Masterworks based on how much they think it’s valued.

After you’ve bought it, you solely rely on them to tell you how much they think it’s valued right now.

That does not sound right to me.

Now, having said that, there are also pros of art investing with Masterworks.

If you are very keen on art investing and have a deep understanding of how art investing works and how to value art, then Masterworks makes it very easy and simple to start investing in art with as little as $1,000.

Its platform is very easy to use and it also provides educational resources on art investing.

Risks Related To Masterworks Art Investing

When it comes to any form of investing, it is always prudent to analyze the downside risks first instead of only focusing on the potential (advertised) upside.

There are quite a number of risks involved in art investing with Masterworks.

First of all, you need to know that Masterworks issuers do not generate revenue.

So, if you invest in any of them, you will only recognize a (positive or negative) return on your investment if the painting is sold or you are able to sell your shares on Masterworks’ secondary market (by the way, it’s extremely illiquid)

In other words, you have to be mentally prepared to hold your art investment for an indefinite period.

If you think that you might need to take out your money for retirement or kids’ college tuition in the foreseeable future, art investing might not be ideal for you.

Secondly, Masterworks is the first of its kind to make art investing accessible to individual investors.

Thus, its business model is not proven and may fail.

If Masterworks as a business fails, Masterworks issuers may be compelled to auction off artwork at an inopportune time, which could result in losses.

Thirdly, each Masterworks issuer is undiversified, thus it could be highly risky.

This is because 100% of the investment is either concentrated in a single artwork or a collection of artwork.

Fourthly, there is no active public market to trade Masterworks issuer shares, so it’s extremely uncertain (ie. extremely unlikely) for you to trade your shares.

Although Masterworks provides a bulletin board as a way to connect potential buyers and sellers in the secondary market to buy and sell shares, there is almost close to zero liquidity there as you can see below.

Also, Masterworks DOES NOT facilitate any transactions in the secondary market, nor does it provide liquidity.

If you are lucky to find a buyer or seller, you will have to contact them yourself and arrange for the trade to be settled with a third-party bank.

As you can see, it’s very troublesome and inconvenient.

Lastly, there are a number of risks in art investing, including

- claims with respect to authenticity or provenance

- physical damage due to improper storage, poor workmanship, accidents, theft, natural disasters, fire, etc.

- legal challenges to ownership

- fraud

Masterworks Art Investing Vs Stock Investing

So, how does Masterworks art investing compare with stock investing?

Personally, I prefer stock investing.

Here’s why.

When you buy stocks, you are buying businesses.

Unlike art, good and profitable businesses generate earnings month after month, quarter after quarter, and year after year.

So, you are basically buying the future earnings that the businesses can generate.

Art does not generate earnings.

Personally, I feel more comfortable investing my money in great money-making businesses than in art because I could at least estimate the value of the business with confidence.

With art, I don’t know any way of valuing it.

On top of that, I know for certain there are a lot of great investors who have made money by investing in great businesses in the long term.

Normal people who follow the right investing strategy such as value investing could grow their wealth over time such as the Janitor, Ronald Reed, who amassed $8 million over time by investing in great businesses and holding them for a long time.

That’s proven.

However, I have yet to know ordinary people just like you and me who have amassed a great fortune by investing in art.

In fact, Warren Buffet once used the “Mona Lisa” to explain why art is a terrible investment many years ago.

Warren Buffet said that France would have made 1 quadrillion if it had invested instead of buying the “Mona Lisa”.

“Buffett noted that Francis I, the former king of France, bought Leonardo Da Vinci’s “Mona Lisa” in 1540 for 4,000 gold crowns, or the equivalent of $20,000. If the monarch had plowed that money into an investment generating a modest after-tax return of 6% a year, the country’s coffers would be overflowing with more than $1 quadrillion by 1963, or 3,000 times its national debt. Meanwhile, the “Mona Lisa” was insured at a value of $100 million in 1962.”

So, there you have it.

Personally, you will have a much better chance of growing your wealth through investing in good businesses than buying art.

Here’s a list of stock research platforms that I use to find good businesses to invest in:

Motley Fool Stock Advisor is focused on giving stock recommendations that are high-quality companies with long-term growth potential, which suits my investment philosophy.

The reason why I subscribe to Stock Advisor is to get stock ideas as Motley Fool has a proven record of finding stocks with massive upside potential.

Personally, I don’t buy every single stock recommendation.

What I do is that if I find any interesting stock pick, I will do my own research again.

First of all, let’s take a look at their track record as of 5th Sep 2023.

Below is the performance comparison between Motley Fool Stock Advisor and S&P 500 between 2002 and 12th March 2024.

As of 12th March 2024, average Motley Fool Stock Advisor recommendations have returned over 651% since inception while the S&P 500 has returned 150%.

In short, the Motley Fool Stock Advisor has outperformed the market 3 to 1.

But, what about its individual stock picks?

This metric is important because I might not be buying every single stock recommendation made by the Motley Fool Stock Advisor.

Below is a table that shows you the performance of individual stock picks over the years.

As of 6th September 2023, Motley Fool Stock Advisor has had 173 stock recommendations with 100%+ returns.

[Past performance is no guarantee of future results. Individual investment results may vary. All investing involves risk of loss.]

Will the Motley Fool Stock Advisor always be right about their stock recommendations?

No, because no one can be right about their stock picks 100% of the time.

Let me sidetrack a bit here.

If any stock picking service tells you that they have a close to 100% success rate on their stock picks and can guarantee you high investment returns, you should definitely stay away.

Even Warren Buffet has loss-making stocks in his portfolio, but he still achieves above-average returns because a few big gainers in the portfolio can make up for the under-performers.

What I like about the Motley Fool Stock Advisor is that they are very open and transparent about their bad investments.

As a member, I can see the performance of ALL its past and current stock recommendations (even for closed positions).

For some other stock-picking services that I’ve tried, they don’t publish the performance of all their past and current stock recommendations, so it’s not easy for you to find out their true track record.

So, if you are thinking of getting into stock investing, I highly recommend the Motley Fool Stock Advisor because I think there are a lot of well-researched stock recommendations.

In terms of pricing, Motley Fool Stock Advisor is also much more affordable.

Usually, its annual subscription is $199.

Right now, there’s a special limited-time $89 offer* for new members for the first year when you click the link here to try it out for 30 days with a Membership-Fee-Back Guarantee. (*Billed annually. Introductory price for the first year for new members only. First-year bills at $89 and renews at $199)

So, for $89 a year- that’s just $1.7 a week – you can gain unlimited access to their library of expert stock recommendations which are carefully selected to help you grow your wealth.

Limited Time: Special $89 Stock Advisor Introductory Offer For New Members

Leave a Reply