DISCLOSURE: THIS POST MAY CONTAIN AFFILIATE LINKS,MEANING That I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS, AT NO COST TO YOU. PLEASE READ FULL DISCLOSURE HERE

Are you looking for Tom Gardner’s stock picks?

How exactly does Tom Gardner pick his stocks?

Can you really trust his stock picks?

How have his stock recommendations performed over the years?

Tom Gardner Background

So, who is Tom Gardner?

Tom Gardner, together with his brother David Gardner, founded Motley Fool back in 1993.

Motley Fool is a financial publishing company that has been around for almost 30 years.

As of 2019, The Motley Fool also has operations in the US, United Kingdom, Australia, Canada, Germany, Hong Kong, and Japan with a total number of 300 employees.

Tom is also a best-selling author of a few investment books such as “The Motley Fool Investment Guide”, “Million Dollar Portfolio”, and “Rule Breakers, Rule Makers.”

Tom Gardner’s Investing Beliefs

So, what are Tom Gardner’s investing beliefs?

First of all, Tom Gardner believes that you are better off investing in stocks because it has always performed better than all the other asset classes (e.g. real estate, bonds, gold, etc) in the long term.

Secondly, he believes that you should always manage your investment yourself instead of putting your money in the seemingly safe yet often underperforming mutual funds.

Why?

Because there is no other person who will care more about your financial success than yourself.

Another reason is that research has shown that the majority of mutual fund managers cannot beat the market.

On top of that, you are paying management fees every single year, regardless of whether the fund is making you money or not.

These annual management fees can significantly lower your returns in the long term.

However, if you prefer not to do investment research yourself and manage your investment actively, Tom thinks that it’s wise to invest your money in funds that are managed by fund managers with a good track record and low fees or Vanguard ETFs.

When it comes to investing in stocks, here’s what Tom Gardner believes:

- Invest in the long term and only invest the money that you don’t need for the next 3 to 5 years

- Build a balanced investment portfolio based on your financial situation, goals and risk profile

- Allocate a portion of your portfolio to blue-chip companies (because these companies are more stable and less risky than smaller companies)

- Allocate a smaller portion of your portfolio to small-cap stocks (because earnings grow faster in small-cap companies and thus the long-term returns would likely be much higher)

Last but not least, there is always risk involved when it comes to investing.

Taking zero risks is not going to help you grow your wealth.

On the other hand, taking reckless risks is not going to help you either.

For example, you invest in dubious penny stocks that are cheap but extremely risky and volatile.

So, you should always consciously take on smart risks by doing your due diligence because this remains the best way to succeed in investing.

Tom Gardner’s Investing Strategy

So, how exactly does Tom Gardner pick stocks for his personal investment portfolio?

Tom Gardner recommends business-focused investing, seeking out great and amazing businesses with growth opportunities.

And he approaches the market with a “business owner” mentality rather than a “stock buyer” mentality.

Before investing in any business, it is important to ask where the company will be in the next 5 to 10 years.

Once he has found a great business to invest in, he thinks it is good to hold these stocks for a minimum of 5 years and add money regularly to them.

So, when it comes to evaluating if the business is worth investing in, here are five tenets of great investments designed and personally used by Tom Gardner:

#1. Culture

The first one is company culture.

So, what does Tom Gardner mean by company culture?

It is how the company treats its employees, customers, suppliers, and stakeholders.

For Tom Gardner, companies that focus on treating all their key constituents well tend to thrive over the long term.

Now, how do you determine if a company has a positive culture?

Here are a few questions that you can ask:

- Is the company ownership structure vested and aligned with the interests of the shareholders?

- Is there a higher purpose that inspires long-term growth?

- Is there evidence that when the business wins, the customer, the employees, and the world also wins?

- Are there high levels of employee engagement and retention?

#2: Strategy

The next one is the company’s strategy.

So, what does Tom Gardner mean by that?

When it comes to analyzing the company’s strategy, Tom Gardner looks at the following areas:

- What competitive advantages does the company have?

- Does it offer the best solution to its customers in the industry? (i.e. what’s the level of customer loyalty )

- Does it have pricing power? (i.e. does the business have the ability to raise prices steadily without driving customers away?)

- What is the size of the market opportunity? (e.g. the size of the market opportunity of Apple. Inc is definitely much bigger than that Manpower Group (which offers staffing and outsourcing services).

#3: Financials

The third one is the company financials.

A company can have a great culture and a winning strategy, but if its financials are a mess, it won’t be a good investment.

When it comes to examining a company’s financials, many people focus on revenue and net income.

For Tom Gardner, here are the most important numbers to watch:

- Sales growth (i.e. is it generating more sales year on year?)

- Return on equity (preferably more than 10%)

- A high but sustainable profit margin

- A healthy balance of cash and long-term debt

#4: Risk

The fourth one is risks.

So, what are the potential risks that the business could face in the future?

Everything might look good right now, but things could change (for the worse).

One of the potential risks that every business faces is industry disruption risk.

Newspapers have been rapidly replaced by online media and blogs.

Uber and Lyft are competing with the taxi industry for market share.

Traditional television is losing market share to online streaming companies such as Netflix. (Personally, I have stopped watching cable TV for years and don’t think I will ever do that in the future)

So, it’s important to think about all the ways that businesses can run into trouble and assess the likelihood of each.

Then, you ask yourself, what has the company done to mitigate the risks?

As you are putting your hard-earned money into these stocks, you have to think about what could go wrong.

Here’s a list of other potential risk factors that Tom Gardner would look at:

- Leadership succession planning

- Diversification of customers

- Diversification of suppliers

- Regulatory threats

#5: Valuation

The last one is valuation.

So, how much does the market think the company is worth?

Is it being over-confident or underestimating the underlying business and its future growth potential?

It’s an important metric to consider, but if you can find truly great businesses to invest in, it won’t matter that you purchased Amazon shares at $100 or $200. (Amazon’s share price is $3,297 as of the date of my writing)

This is because you are taking a long-term view of the investments.

So, how exactly does Tom Gardner arrive at the business valuation?

First, Tom Gardner would focus on per-share cash flow and where it would be in the next five years.

Why cash flow?

This is because cash flow is not difficult for accountants to manipulate (yes, accountants have a lot of tricks to manipulate revenue).

By looking at how much cash flow the business can generate, you get a real picture of how the business is doing.

Also, as a long-term investor, Tom Gardner thinks that it is important not to get affected by the short-term noise in the market.

For example, the Facebook share price was $38 when it went on IPO and then went to as high as $70 before tanking to a low of $24.

What happened?

Back then, people were portraying Mark Zuckerberg in a very unfavorable light after the movie The Social Network.

Also, Facebook was not profitable as Mark Zuckerberg made the decision to go through the costly process of retraining developers from desktop to mobile because desktop usage is collapsing and mobile is the new trend.

This is a strategic long-term business decision at the expense of short-term profit.

But, many investors were just focused on the short term and missed the big picture.

This exactly gave long-term investors the opportunity to buy great businesses at dirt-cheap prices.

In fact, Tom Gardner, who had been watching the Facebook stock for a while, recommended Motley Fool Stock Advisor members to buy Facebook shares when it tanked to the low of $24.

Now, let’s go back to how Tom Gardner arrives at the valuation of every business.

Once you have estimated the average per-share cash flow for the next 5 years, then you apply a multiple to it.

That will give you the equity portion of the business.

Multiple is how many times the per-share cash flow that you are willing to pay for the business.

For example, let’s say Facebook’s per-share cash flow is $8.

Are you willing to pay $80 per share( i.e. a multiple of 10) or $240 per share ( i.e. a multiple of 30)?

If you expect the per-share cash flow to grow steadily every year, then you would be willing to pay a higher multiple.

Once you estimate the equity portion of the business, then you add all the cash and subtract the debt to arrive at the business valuation.

How Tom Gardner Applies His Stock Picking Strategy

Let’s use Google as an example to show how Tom Gardner applies his investment strategy in his stock selection.

Tom Gardner thinks that Google is one of the greatest companies in America, with an extremely data-centric culture.

Google measures everything and surveys its employees frequently in an effort to understand deeply what drives each person.

It uses data and technology to connect with each employee in ways that other large companies cannot.

And how do Google employees feel about working for Google?

According to Forbes, Google is ranked first on Forbes’ Global 2000 list of the World’s Best Employers for the third year in a row.

To Tom Gardner, this two-way connection between employee and employer is a strong indicator that long-term value is going to be created.

This is also one of the five tenets of great investments that Tom Gardner talked about earlier – “Culture”.

Next, let’s look at Google’s strategy.

What’s Google’s competitive edge?

Its competitive edge manifests in the following areas:

- The advantage of scale (i.e. the dominance of Google’s search engine)

- Google’s intellectual property—specifically, its search engine algorithm

- Google’s brand name

What about Google’s financials?

Below is the graph of Google’s annual revenue from 2002 to 2019.

What about Google’s profit margin?

Google’s profit margin has been consistently staying at around 20%.

What about its balance sheet?

Does it have a high level of debt?

As of the end of the 2019 fiscal year, Google’s D/E ratio was 0.08, indicating an extremely low debt-to-equity ratio.

In fact, over the 15-year period from 2005-2020, Google’s Debt/Equity ratio has never risen above 10%.

Now, let’s take a look at its cash.

Its cash and investments have grown massively in the last 10 years as shown in the graph below.

Now, what about risks and valuation?

The biggest risk that Google faces is regulatory risk.

Given the company’s huge market share in search and in its Android mobile operating system, regulators in the US and Europe are monitoring Google’s business practices for anti-competitive behavior.

This in a way proves that Google has too strong a competitive edge in its industry.

Tom Gardner actually recommended Google many years ago and has re-recommended it to Motley Fool Stock Advisor members.

Now, let’s take a look at the Google share price chart.

Its share price has been increasing steadily over the years.

Tom Gardner’s Strong Conviction Stock Picks

Here are two of Tom Gardner’s stock picks for 2022.

Arista Networks is a pioneer in software-driven cloud networking solutions, and Arista’s technology helps companies move vast quantities of data over the Internet at lightning speeds. Its products include both hardware and software.

Here is the list of reasons why he likes this company:

- The company’s differentiator is the software that controls the hardware, namely its Extensible Operating System (EOS).

- Potential market expansion (e.g. campus networking, routing, and CloudVision)

- Rock-solid financials

- The company has incredible leadership with a long-term focus

- Both the CEO and Founder control about 18% of the company’s shares

However, there are also potential risks involved:

- Networking technology is a competitive field, and Arista could always be disrupted. (But it’s taking precautions against that by continuing to spend about 20% of its total revenue on research and development)

- Arista has a few large customers that have historically accounted for a disproportionate share of its revenue.

Airbnb operates an online vacation and travel rental lodging platform.

Here is the list of reasons why he likes this company:

- Airbnb continues to innovate and improve its platform

- Most recent quarter results are very solid (e.g. it reported over 102 million nights and experiences booked, surpassing pre-pandemic levels and representing a 59% year-over-year increase. The company generated $1.2 billion in free cash flow and saw gross nights booked move 32% higher than 2019 levels)

- The near-term future looks good with strong demand for travel

- Long-term stays continue to be the fastest-growing category by trip length and are at an all-time high

However, there are also potential risks involved:

- If there is an economic downturn, its debt service might become an issue because it has over $45.5 billion in debt on its balance sheet.

- If there is a pandemic resurgence, the post-pandemic recovery in travel would falter and the company would likely suffer.

- If inflation remains high, people could cut down their travel budgets

Motley Fool Stock Advisor Stock Pick Performance

As you might know, Tom Gardner is part of Motley Fool’s Stock Advisor investment team.

First of all, let’s take a look at their track record as of 12th March 2024.

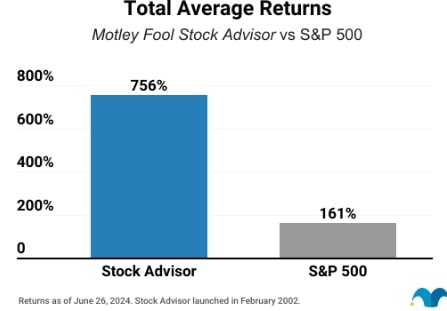

Below is the performance comparison between Motley Fool Stock Advisor and S&P 500 between 2002 and 26 June 2024.

As of 26 June 2024, average Motley Fool Stock Advisor recommendations have returned over 756% since inception while the S&P 500 has returned 161%.

In short, the Motley Fool Stock Advisor has outperformed the market 4 to 1.

But, what about its individual stock picks?

Below is a table that shows you the performance of individual stock picks over the years.

As of 6th September 2023, Motley Fool Stock Advisor has had 173 stock recommendations with 100%+ returns.

[Past performance is no guarantee of future results. Individual investment results may vary. All investing involves risk of loss.]

So, how much does Motley Fool Stock Advisor cost?

Usually, its annual subscription is $199.

Right now, there’s a special limited-time 50% OFF offer* for new members for the first year.

Leave a Reply